Inflation Is Here. Now, What Should Investors Do?

It’s no secret at this point that inflation is back. The Labor Department reports that consumer prices rose 0.9% in October versus September. That’s 6.2% higher than 2020. You’ve noticed it at the gas pump and checkout line for sure, but even if you exclude food and energy, prices are up nearly 5% versus a year ago. That’s the biggest jump in 30 years.

Economists and the Federal Reserve have been saying this is a temporary thing. The pandemic unexpectedly accelerated demand for a lot of goods while factory capacity was reduced, creating shortages. At the same time, there are supply constraints, such as the lack of truck drivers and dock workers and not enough semiconductors— which are inside a lot more products than you probably realize—to go around.

But nothing is certain. The labor market may have shifted. With people doing jobs we took for granted, they would keep doing trying other work. Another risk is that, to an extent, prices could keep rising just because consumers believe prices will keep rising. That is, if people think prices are going to rise, they’ll buy now, further exacerbating the supply-and-demand issues.

Investors, especially retirees or those close to being retirees, need to pay attention. Shrugging this all off as being a short-term phenomenon may work out for you, but it could also blow up in your face.

There are only so many such explosions an older investor can handle. Longer-term inflation is one of the most fearsome foes of a retirement plan. It’s true that Social Security tends to keep up with inflation, at least over the long term, so that’s a plus. And if you’re lucky enough to have a pension, it probably does as well.

But there’s no salary income —which almost always at least matches inflation growth year to year— to keep you going. Inflation is the enemy if you have investments and intend to draw down on those investments to cover your spending. You’ve likely chosen an annual withdrawal rate on those investments assuming, say, a 2% or 3% inflation rate. If inflation is more like 4% or 5%, that withdrawal rate will probably have to increase unless you can tighten the belt a bit.

It’s prudent for older investors to prepare for the possibility that higher-than-normal inflation will be with us for a while. Here are a few things to try.

What If?

The WealthTrace financial planning application can help you simulate the effects of higher inflation. It takes a look at your portfolio and lets you see what could happen if inflation runs higher than expected for a longer period of time than expected. (Spoiler alert: It’s not something you want to happen.)

The program can run this change through a Monte Carl simulation. Monte Carlo, in a nutshell, runs a whole lot of simulations based on historical total returns, standard deviations, and correlations of the asset classes in a portfolio. Instead of saying, “if my portfolio returns X% per year, I should be good,” which is not very real-life. Monte Carlo throws wrenches into the works, such as bear markets, recessions, and stock market bubbles.

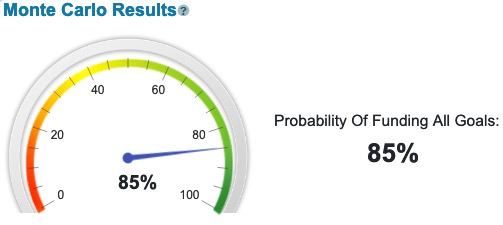

Here’s what we mean. This couple in their late 50s has nearly $2 million in investments and assumes 3% inflation annually. Without getting into the details of what asset classes they own, we’ll just say they have an 85% probability of funding all of their retirement goals, according to Monte Carlo.

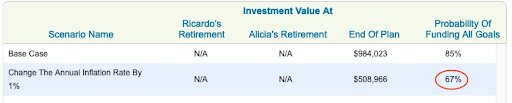

An 85% number is good, if not great. But if we increase the assumed inflation rate by 1% as is shown in the image a few paragraphs above, we start to get into the red-alert territory:

The N/As are there because they’re already retired. The key number here, though, is 67%. Nobody wants to be heading into retirement with only a two out of three chance that they’re going to make it.

What will be necessary to account for this possibility is probably a combination of things. The couple could reduce their projected spending. They could also consider reworking their portfolio’s asset allocation to see what assets would hold up in an inflationary environment. WealthTrace lets them try these things.

Changing It Up

Speaking of asset allocation: What should you do with an investment portfolio if you think inflation will be with us for a while?

We wish we could give you a one-size-fits-all answer to this question, but we can’t. Traditionally investors have turned to hard assets, such as natural resources, as an inflation hedge. Gold is one as well. In recent years cryptocurrency, too. There are no guarantees, though, and these can be highly volatile assets. If you move some money into them, don’t go overboard.

Sometimes people think of bonds as a shelter against just about anything that could go wrong with a portfolio. But they’re no magic shield against inflation, especially if they’re long-term bonds. That’s because, with inflation trending upward, current bond yields will almost be lower than the yields of issued bonds as inflation goes up, so ‘older’ bonds will be worthless.

There’s an interesting flavor of bonds known as Treasury Inflation-Protected Securities, or TIPS. It has a built-in hedge against rising interest rates, which tend to follow inflation. It definitely has its issues, such as the potential for being taxed on gains your never take possession of. However, as bond investments go, they are probably inflation-cowed investors’ best bet.

As for the equity part of your portfolio, you probably don’t want to start making wholesale changes just because inflation is a threat. If inflation persists, companies will find ways to pass the buck to consumers eventually. Their profits (and stock) won’t always take a big hit.

So if you do decide some TIPS or hard assets should be part of your portfolio, it doesn’t mean the rest of the portfolio should need a lot of massaging.

Situational Awareness

Everybody’s situation is different, of course. If you depend primarily on income outside traditional stock and bond-market investments, for example, a lot of this doesn’t apply. Or, if you can vary your spending in retirement by reducing spending in hard times and maybe living it up in good times, you might be able to shrug off inflationary fears.

The bigger-picture truths remain. Whatever happens with inflation, the most important things are your risk tolerance and your goals for retirement. Be aware of inflation, keep an eye on it, and know what harm it can do, but don’t let it panic you.

Read More:

- Which Retailers Are Open / Closed on Thanksgiving 2021?

- 5 Supermarket Psychological Tricks That Make You Spend More

- Save Money with These Frugal Thanksgiving Menu Ideas

If you enjoy reading our blog posts and would like to try your hand at blogging, we have good news for you; you can do exactly that on Saving Advice. Just click here to get started. Check out these helpful tools to help you save more. For investing advice, visit The Motley Fool.

Comments