Tweet

Tweet

Hi Guys,

Usually when the default rate for various kinds of debts rise (car loans, auto loans, mortgages, etc.) thats a red flag in terms of economic growth. Well, it looks like loan defaults are starting to creep up again, at least according to the NY Post.

Source: NY Post

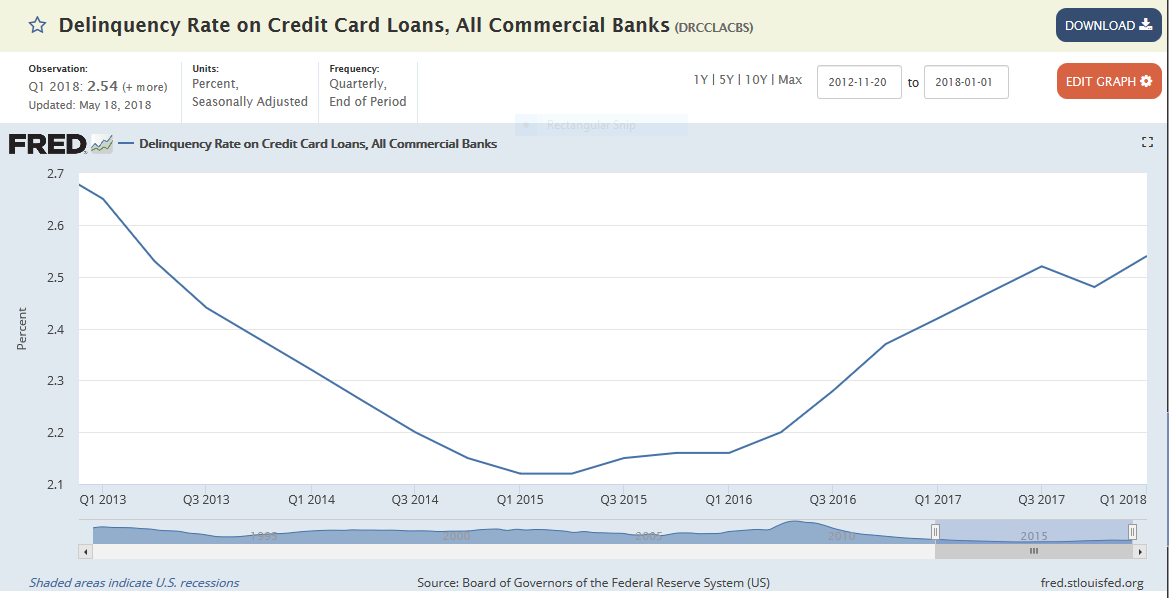

Data from the St. Louis fed says pretty much the same thing. Default rates have been creeping up since 2015.

Source: St. Louis Fed.

So I guess the question is: is a red flag for a recession, or is pretty much back to business as usual?

Usually when the default rate for various kinds of debts rise (car loans, auto loans, mortgages, etc.) thats a red flag in terms of economic growth. Well, it looks like loan defaults are starting to creep up again, at least according to the NY Post.

�I would say that credit card defaults is definitely a cause for concern,� says Joe Resendiz, an analyst with ValuePenguin, which tracks the credit industry.

Resendiz noted the recent second-quarter net credit card default numbers rose for Bank of America and JPMorgan. In an otherwise rosy report, the amount of in-default charge card bills rose by 10 percent and 9 percent, respectively, compared with the same period in 2017.

Resendiz noted the recent second-quarter net credit card default numbers rose for Bank of America and JPMorgan. In an otherwise rosy report, the amount of in-default charge card bills rose by 10 percent and 9 percent, respectively, compared with the same period in 2017.

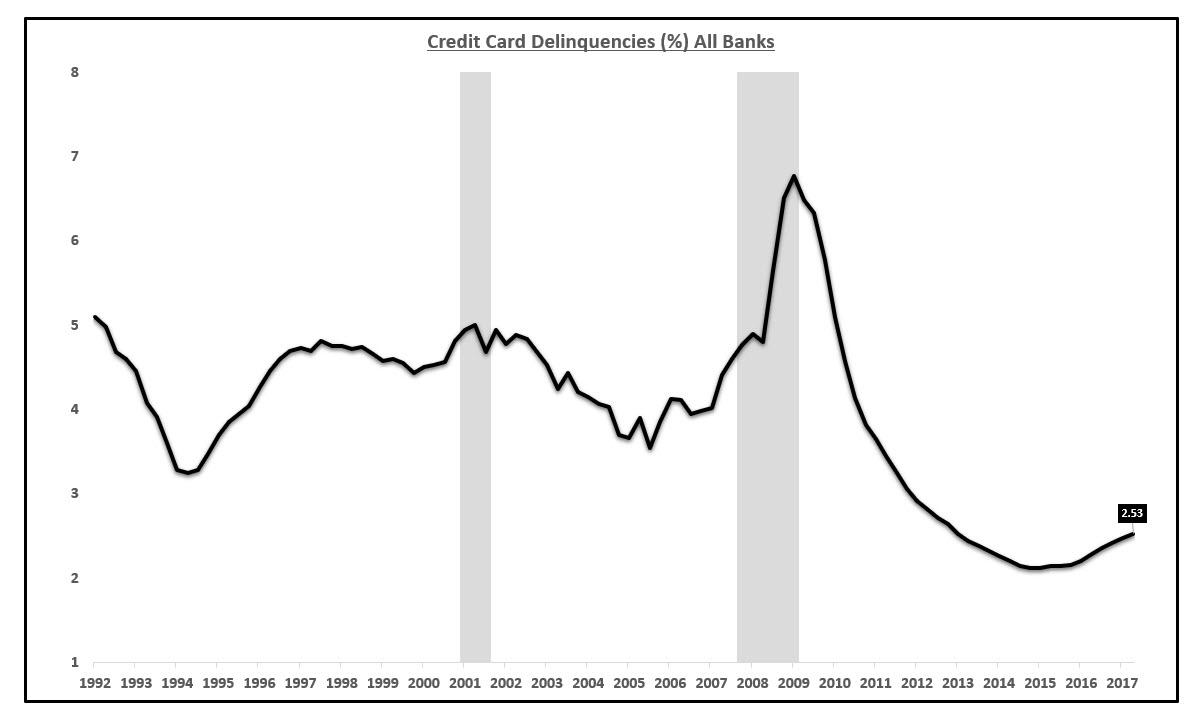

Data from the St. Louis fed says pretty much the same thing. Default rates have been creeping up since 2015.

Source: St. Louis Fed.

So I guess the question is: is a red flag for a recession, or is pretty much back to business as usual?

.

.

Comment